What is Pledging of Shares ? [Dangers for Indian Investors]

What is pledging?

Pledging is equivalent to taking a bank loan against the shares as collateral. Similar to taking a bank loan against property, investors can take a bank loan against their shares.

These loans can be taken by regular shareholders (like you and me) or by the promoters of the company. Pledging done by regular shareholders has no significance to us but if done by promoters, it certainly does.

Pledging by promoters

Here’s how pledging works:

Let’s say, promoter of a company needs money -either for personal or business needs. He goes to a bank or an NBFC and puts X number of his shares as collateral (market value ₹100 crores). These loans typically have a tenure of one to three years and the collateral requirement is quite high: about 2 to 3 times of loan amount. In this case, let’s say the bank lends him ₹40 crores.

What happens from here depends on how the share performs and the ability of the promoter to keep up with the interest obligations.

What can go wrong?

A considerable fall in share price can create a bit of a situation.

Banks are supposed to keep the collateral amount higher than the loaned amount. It means that the market value of the pledged shares should be greater than the loaned amount (₹80 crores)

A considerable fall in the share price will bring the market value of the pledged shares down. To keep the margin (of ₹60 crores) intact, the bank would ask the promoter to either provide a cash payment or additional shares. If the promoter can meet the obligation, there are no issues, but if he can’t, then the bank has full authority to sell the shares in the open market and recover the lent amount. Else, the promoter himself can sell some of his un-pledged shares to pay the bank for the shortfall.

A famous case when a bank sold the shares in the open market is that of SBI Bank selling shares of United Spirits to recover the money that Vijay Mallya owed them.

Why should investors be concerned?

After all, isn’t this affair between the promoter and the bank? Why are we bothered with all this?

Remember that the number of shares pledged is no small change and their value typically runs into hundreds of crores. By the basic equation of supply and demand, when the supply goes up, the prices come down. So, if the bank does decide to sell that many shares in the open market, it will cause a huge supply glut, causing the price to fall sharply.

How to check for pledging?

Higher pledging is a bad reflection of the promoter’s ability to raise funds. Why else would anyone take loans with such stringent margin requirements and negative repercussions on a stock’s performance?

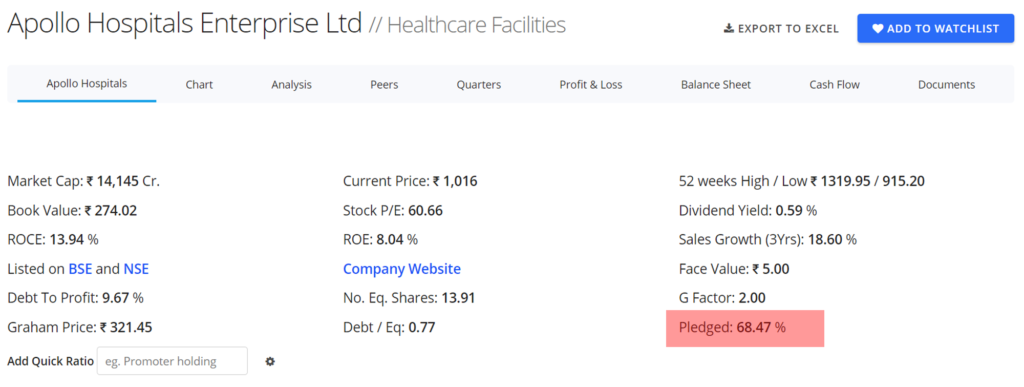

Therefore, investors should always check for the promoter’s pledge. It can be easily found on popular websites such as MoneyControl or screener. in. For example, here are the pledging stats for Apollo Hospital (from screener. in). It shows that 68.47% of the promoter’s shares are pledged.

How much pledge is too much?

An ideal case would be no pledge, good cash flow and a low debt-to-equity ratio. In general, the lower the pledge, the better off the investors.

However, life is not ideal and you would be looking at a stock that is too good to pass just based on a higher pledged percentage. In such cases, it is advisable to stick with stocks where the pledging is less than 25%.

Chapter Summary

- Promoters pledge their shares to the banks in order to raise money for their personal or business needs.

- Banks may be forced to sell the pledged shares in the open market is the promoter can not keep up with the debt obligations.

- A high level of pledged % can create increased volatility in the stock prices.

- Investors should stay away from stocks with high pledged percentage.

![What is Virtual Contract Note [Zerodha]](https://www.vrdnation.com/wp-content/uploads/2023/10/maxresdefault-virtual-note-500x383.jpg)

Leave A Comment