Evaluate Risk and Returns

There is always a trade-off between risk and return.

Types of Investors

We can classify the people basis their risk-taking ability into the following classes:-

- Risk Averse: This type wants to have their capital protected and does not care for the high returns. Typically, they invest in fixed deposits, debt funds and hold cash in hand.

- Moderately Risk Averse: These types of investors are ready to take some risk. Their preferred investment types are exposure in fixed income securities, stocks, real estate, and commodities that track inflation

- Moderately aggressive investors: This type of investor wants to outperform the market index and is not too worried about the market going down. They take more downside risk than the market but expect the same to be compensated by when the markets go up.

- Aggressive Investors: This type likes playing with fire, takes a lot of risks and want to outperform the markets. Their portfolios would normally be made up of growth, small-cap and Sector funds or stocks. If not constructed carefully, the erosion of capital can be heavy and may take years to recoup. However, in the long run, these are the type of investors who gain the most.

Though these are the general types few other factors decide our investment strategies.

- Risk Tolerance: This is nothing but the amount of risk a person can tolerate. I might be young but if I want my money to be safe I would still put it in the bank no matter what. I might not be the kind of person who can handle uncertainty. This however generally changes with age, income and the goals I might have set for myself.

- Risk Capacity: This is the amount of risk one should take to reach a particular financial goal.

People are different and so are their investment strategies. Whatever kind of style fits, one should do enough research before investing their hard-earned money into any asset class.

Investment Horizon

Now let’s have a look at what should be your time horizon for the investment and does the investment made for a longer time gives a better result? The time horizon for investment means the length of time until you need to withdraw your money. Knowing this is very important as this will decide which instrument you should be investing in.

Here are some very rough definitions of those time horizons and associated risk levels. Keep in mind that these are very arbitrary and the definitions are not standard.

- Short Term: As a general rule, short-term goals are those less than 5 years in the future. With a short-term horizon, if a drop in the market occurs, the date on which the money will be needed will be too close for the portfolio to have enough time to recover from the market drop. To reduce the risk of loss, holding funds in cash or cash-like vehicles is likely the most appropriate strategy. Money market funds and short-term certificates of deposit are popular conservative investments, as are savings accounts.

- Medium-term: Medium or Intermediate-term goals are those that are 5 to 10 years in the future. At this range, some exposure to stocks and bonds will help grow the initial investment’s value, and the amount of time until the money must be spent is far enough in the future to permit a degree of volatility. Balanced mutual funds, which include a mix of stocks and bonds, are popular investments for intermediate-term goals.

- Long-Term: Long-term goals are those more than 10 years in the future. More conservative investors may cite 15 years as the time horizon for long-term goals. Over long-term periods, stocks offer greater potential rewards. While they also entail greater risk, there is time available to recover from a loss.

Now here is an example so that the risk associated with the time horizon can be appreciated. Imagine that Mr X started investing at the age of 25. Since age was on his side he put almost 90% of the savings in the stocks market. He was to retire at 65 years and so there were 40 years of savings (I am sure he saved a lot) However, just before he was to retire, the stock market plunged eroding his savings by almost 50%. So if the value of the stocks he was banking on was Rs.1cr, after the market plunge, it became Rs.50 lacs. Can he now wait for the next 10 years for the market to recover? Remember the market crash of the 90s and 2008? It will have a severe impact on his retirement years.

Conclusion

So how do we evaluate the time horizon and the risk associated with them? Well, there are no hard-and-fast rules, however, some understanding of the time frame when you need the money parked in the savings will help you decide which investments are appropriate for various timelines.

You also need to understand that in the short term volatility is a bigger risk than it is in long term. If Mr X of our earlier example faced the market crash when he was 40 years old he need not worry as he has 25 years still to recover so it is not a big danger. So placing some parameters and knowing when you will need the money will help you decide on your investment goals.

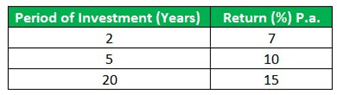

The risk-return trade-off that we talked about can be understood through the graph given below. This clearly shows that the longer the investment is held higher the returns will be.

Courtesy Wallstreetmojo.com

Howdy!

If you’re here for the first time, let’s get introduced.

VRD Nation is India’s premier stock market training institute and we (Team VRD Nation) are passionate about teaching each and every aspect of investing and trading.

If you’re here for the first time, don’t forget to check out “Free Training” section where we have tons of free videos and articles to kick start your stock market journey.

Also, we got two awesome YouTube channels where you can continue the learning process.

Must-Read Articles

How to Recover from a Big Trading Loss?

Secret Weapons of Professional Traders

7 Habits of Highly Effective Traders

7 Reasons Why Traders Love Options

The Biggest Lie About Intraday Trading

Top 5 Books on Technical Analysis

Evaluate Risk and Returns

There is always a trade-off between risk and return.

Types of Investors

We can classify the people basis their risk-taking ability into the following classes:-

- Risk Averse: This type wants to have their capital protected and does not care for the high returns. Typically, they invest in fixed deposits, debt funds and hold cash in hand.

- Moderately Risk Averse: These types of investors are ready to take some risk. Their preferred investment types are exposure in fixed income securities, stocks, real estate, and commodities that track inflation

- Moderately aggressive investors: This type of investor wants to outperform the market index and is not too worried about the market going down. They take more downside risk than the market but expect the same to be compensated by when the markets go up.

- Aggressive Investors: This type likes playing with fire, takes a lot of risks and want to outperform the markets. Their portfolios would normally be made up of growth, small-cap and Sector funds or stocks. If not constructed carefully, the erosion of capital can be heavy and may take years to recoup. However, in the long run, these are the type of investors who gain the most.

Though these are the general types few other factors decide our investment strategies.

- Risk Tolerance: This is nothing but the amount of risk a person can tolerate. I might be young but if I want my money to be safe I would still put it in the bank no matter what. I might not be the kind of person who can handle uncertainty. This however generally changes with age, income and the goals I might have set for myself.

- Risk Capacity: This is the amount of risk one should take to reach a particular financial goal.

People are different and so are their investment strategies. Whatever kind of style fits, one should do enough research before investing their hard-earned money into any asset class.

Investment Horizon

Now let’s have a look at what should be your time horizon for the investment and does the investment made for a longer time gives a better result? The time horizon for investment means the length of time until you need to withdraw your money. Knowing this is very important as this will decide which instrument you should be investing in.

Here are some very rough definitions of those time horizons and associated risk levels. Keep in mind that these are very arbitrary and the definitions are not standard.

- Short Term: As a general rule, short-term goals are those less than 5 years in the future. With a short-term horizon, if a drop in the market occurs, the date on which the money will be needed will be too close for the portfolio to have enough time to recover from the market drop. To reduce the risk of loss, holding funds in cash or cash-like vehicles is likely the most appropriate strategy. Money market funds and short-term certificates of deposit are popular conservative investments, as are savings accounts.

- Medium-term: Medium or Intermediate-term goals are those that are 5 to 10 years in the future. At this range, some exposure to stocks and bonds will help grow the initial investment’s value, and the amount of time until the money must be spent is far enough in the future to permit a degree of volatility. Balanced mutual funds, which include a mix of stocks and bonds, are popular investments for intermediate-term goals.

- Long-Term: Long-term goals are those more than 10 years in the future. More conservative investors may cite 15 years as the time horizon for long-term goals. Over long-term periods, stocks offer greater potential rewards. While they also entail greater risk, there is time available to recover from a loss.

Now here is an example so that the risk associated with the time horizon can be appreciated. Imagine that Mr X started investing at the age of 25. Since age was on his side he put almost 90% of the savings in the stocks market. He was to retire at 65 years and so there were 40 years of savings (I am sure he saved a lot) However, just before he was to retire, the stock market plunged eroding his savings by almost 50%. So if the value of the stocks he was banking on was Rs.1cr, after the market plunge, it became Rs.50 lacs. Can he now wait for the next 10 years for the market to recover? Remember the market crash of the 90s and 2008? It will have a severe impact on his retirement years.

Conclusion

So how do we evaluate the time horizon and the risk associated with them? Well, there are no hard-and-fast rules, however, some understanding of the time frame when you need the money parked in the savings will help you decide which investments are appropriate for various timelines.

You also need to understand that in the short term volatility is a bigger risk than it is in long term. If Mr X of our earlier example faced the market crash when he was 40 years old he need not worry as he has 25 years still to recover so it is not a big danger. So placing some parameters and knowing when you will need the money will help you decide on your investment goals.

The risk-return trade-off that we talked about can be understood through the graph given below. This clearly shows that the longer the investment is held higher the returns will be.

Courtesy Wallstreetmojo.com

Leave A Comment